Kempen Real Estate Update: Tracking & Engaging: Our approach to getting Real Estate Paris-Proof

Regional and sectoral differences in Green House Gas management

Earlier we already alluded to various degrees of control a company can have over its assets. As shown in this report from GRESB the amount of control a company has will affect how carbon emissions are booked. This means companies can really only be compared with a quite narrow group of peers.

A few of the best practices in various regions do deserve specific mention. In broad terms, American companies will seek external verification and disclose the exact standard used for their Greenhouse Gas “GHG” measurements more often than companies in other regions. Companies in Hong Kong will be more specific in their policy statements and are very meticulous and transparent on the distinction between policies and short-term tactical objectives. European and Australian companies are more advanced in their quest for sustainability, mainly due to proactive actions by companies, encouraged by governments.

The route to seek improvement with companies is identifying best-in-class examples and holding companies accountable consistently. Being critical of plans yet reasonable and keeping an unwavering eye on 2050 and literal carbon neutrality. Ideally, we look for broad positive changes at the margin.

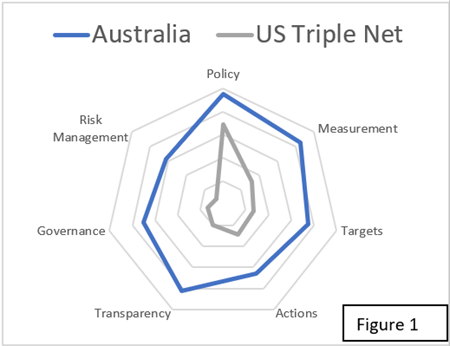

One factor to keep track of is whether companies with less control of their assets will use this as an excuse to not do much. An example of a company that has legitimate worries of lack of control, yet trying to do better is Realty Income Corp. As a triple net lease company, the amount of control is very limited. Despite this drawback, the group has actively started setting up green clauses in their leases in Europe and is rolling out similar practices in the US. These measures are still in their infancy, but given the scale of Realty Income, it will provide the most lagging sector in Real Estate an excellent example of how to do better. Figure 1 on the next page shows that there is still a discrepancy between US Triple net and Australian companies, which are best in class. Clearly, the US Triple Net sector still has a long way to go.

How to be better?

To evaluate companies on sustainability, Van Lanschot Kempen has developed a Carbon Framework to which all companies in the investable universe have been subjected. It is a measure to quantify and track the key performance indicators described earlier. Monitoring the improvements and continuously holding companies accountable is being integrated into the investment process. Using a framework with a predetermined scoring model will aid consistency and comparability.

Realty Income Corp. is a good example of the dual approach one must wield when trying to make companies act and be better. One needs to at simultaneously push the ESG leaders in a subsector to do better pull the laggards towards the example set by said leaders.

Another aspect is to keep top of mind, is a relentless approach with a relationship mindset. Push too hard and relationships with companies can sour; don’t push hard enough and companies will not do what they can. The relationship component is especially relevant in non-listed real estate, as one cannot rely solely on publicly available information in this market, making relationships and dialogue crucial.

Perhaps the most important factor however is to practice what we preach. Not only is it easier to ask companies to do as you do yourself, but it also boosts credibility.

What is left to figure out?

As previously discussed the quest for high-quality consistent ESG data is at this point still ahead of us. Still tracking trustworthy, standardized, externally verified data in line with universal standards like the GHG Protocol will form the basis of standardization. Even so, there are very local aspects to consider like local climate and access to economically feasible renewables. 53% of the companies in our universe have yet to commit to carbon neutrality and 39% of the same companies have no significant GHG targets whatsoever. The battle for climate neutrality is still in its infancy, but Kempen’s Real Assets team is rising to the challenge and hoping to help our investees along in the process.

Even though we realize the overall tone of this piece has been rather skeptical we would like to end on an optimistic note. Companies, technology, and the sciences will become more efficient in preserving our environment, our buildings, and our future. The drive to make our world better will drive economic opportunities, innovation, and, for those who will consider the future, investment returns. We, at Van Lanschot Kempen Real Assets team shall continuously strive to be at the forefront of what will be the most transformative phase for Real Assets in a few generations. We shall do this by supporting Sustainability Leaders that lead, and challenge Sustainability Laggards to catch up, by helping them with their plans and providing them a partnership.

In conclusion, we’ve started this path of sector-wide engagement, because this sector’s potential for decarbonization should not be underestimated.